GLP-1 War of the Words Part II: The Contenders

Amgen and Viking aren’t just joining the GLP-1 race; they’re trying to tell a new story.

Following on my recent narrative analysis of the industry-leading GLP-1 drugs from Lilly (Mounjaro, Zepbound) and Novo Nordisk (Ozempic, Wegovy), I promised a follow-up on two GLP-1 contenders now in Phase 2 and 3 development.

Readers asked for a deeper narrative dive into Amgen's MariTide and Viking Therapeutics' VK2735.

As in Part 1, I’m using the Strategic Narrative Framework and Signal Score diagnostic to evaluate how the contenders tell their story. Both companies are building in the shadow of Novo and Lilly, aiming to carve out differentiation in a market projected to reach $100B by 2030. Rather than copy the current weekly injection playbook, they’re targeting barriers that today’s GLP-1s haven’t solved: weight-loss plateaus, dosing burden, and adherence.

-

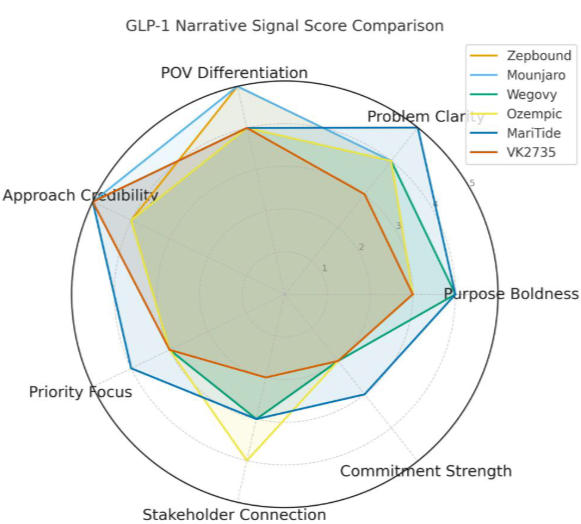

The Signal Scores

My Signal Score™ diagnostic analysis reveals how these contenders are positioning themselves in what’s now Novo and Lilly's sandbox:

Amgen's MariTide: 82/100

Viking's VK2735: 76/100For this analysis, I used

1) Each company's web page for their compound / drug

2) Their 2025 press releases, and

3) One additional anchor document.

For approved drugs like Lilly’s and Novo’s, I used the package insert, the most detailed public-facing drug narrative. For compounds in development without a PI, like Amgen’s and Viking’s, I used their annual report/10k.

I scored each story across the seven narrative dimensions: purpose boldness, problem clarity, point-of-view differentiation, approach credibility, priority focus, stakeholder connection, and commitment strength -- all weighted to 100.

Disruptive Differentiators: Building New GLP-1 Markets

What's striking about Amgen and Viking is that these companies aren’t just joining the GLP-1 race; they’re trying to build a new story, one that skirts the major barriers the leaders haven’t broken through.

Amgen is positioning MariTide around “monthly or less frequent dosing.” That’s a convenience play, true; it’s also a direct solution to the biggest problem to date with GLP-1s: getting patients to stick with their program for the long haul. MariTide has demonstrated “up to ~20% average weight loss at 52 weeks without a weight loss plateau,” directly addressing the wall that frustrates patients on current therapies. In Type 2 diabetes, Amgen also reported ~17% average weight loss at 52 weeks, also without a plateau.

Viking takes an equally bold approach with VK2735's dual-formulation strategy. In a market dominated by injections, they're developing both a weekly injectable and a once-daily oral tablet, which could potentially solve the access barrier that keeps many eligible patients from GLP-1s entirely (many people just don’t like shots). In Phase 2, the oral tablet showed up to ~12.2% mean weight loss at 13 weeks, with a continued downward trajectory.

These aren't incremental improvements competing for market share. They're market-expansion plays.

Amgen: Flipping the GLP-1 Script with GIP Antagonism

With MariTide, Amgen is placing the most audacious scientific bet in the GLP-1 wars, taking the exact opposite approach to dual-agonist therapy as many other players. While Lilly’s tirzepatide (Mounjaro and Zepbound) activates GIP and GLP-1 receptors, Amgen's MariTide activates GLP-1 and blocks GIP signaling.

But I’m not here to parse receptor biology; I’m here to see how companies turn it into story. And MariTide’s approach isn’t just differentiated, it’s a deliberate contradiction of the current GLP-1 gospel. Their preclinical data suggests this “pioneering” (their bold word) combination “had a stronger effect on weight loss than targeting either GLP-1 or GIP receptors alone." If Phase 3 confirms this, Amgen won't just have a competitive drug, they could potentially rewrite the scientific rationale that Lilly and Novo have spent years establishing.

Given the contrarian science they’re pursuing, it’s not surprising that Amgen scores highest in Approach Credibility and Problem Clarity (both 14/15) in my Signal Score analysis, reflecting their innovative science as well as precise narrative construction. Their problem articulation provides specific statistics and barriers, while their communications emphasize MariTide as "the first monthly or less frequently dosed obesity treatment." With a smart nod to their heritage and decades-long reputation, Amgen reinforces that the science is backed by "one of the largest clinical trial programs in Amgen's 45-year history."

Viking: Scientific Strength, Narrative Clarity Gap

Viking's VK2735 demonstrates strong approach credibility in their narrative, scoring 14/15 in my analysis, achieving "Excellent" status. Their dual-formulation strategy shows sophisticated execution planning, with clinical data supporting both approaches. The injectable version achieved ("up to 14.7% weight loss from baseline (13.1% vs. placebo") in their VENTURE Phase 2 trial, while their once-daily oral formulation in Phase 2 showed meaningful weight loss in 13 weeks (up to 12.2% vs. 1.3% placebo).

Viking has successfully positioned VK2735 for a two-pronged approach to the market. Yes, they’re following the dual-agonist playbook, and they’re facing pressure from other oral formulations being advanced by both Novo and Lilly. But they also have an opportunity to build a narrative from the ground up about a flexible patient journey with two separate formulations developed in parallel.

This gives them a powerful story to tell about meeting patients where they are, whether with a familiar shot or the convenience of a daily pill. My Signal Score analysis ( 6/10 on Stakeholder Connection) suggests they’re not yet telling this story in the most effective, patient-friendly way, but the potential is there.

Here’s where Viking's narrative gets challenging. Although the analysis shows "Excellent" Approach Credibility and “Good” POV Differentiation, they have gaps in articulating Problem Clarity (10/15), which limits their narrative impact compared to Amgen's more tightly framed barriers, and decades-old reputation.

Founded in 2012, Viking isn't exactly a brand-new player on the scene, but it lacks the reputation Amgen has built over nearly 50 years. Without that "heritage halo," clarity and stakeholder connections become even more critical. In narrative terms, Amgen gets the benefit of the doubt; Viking has to earn it.

The contrast shows how communication strategy becomes a competitive moat. Amgen leverages its established credibility to tell a confident story about paradigm shifts. Viking must work harder to establish that same credibility through more specific, accountable messaging.

Narrative Resilience Under Fire

Both companies have faced significant tests that spooked markets, and their responses show why narrative resilience is as critical as the data.

In late 2024, MariTide was hit with bone-mineral-density (BMD) concerns that wiped $12 billion off Amgen’s valuation and could have derailed confidence in their dual-pathway approach. But Amgen's response was quick and decisive, publicly addressing the issue head-on, and providing data to refute the concerns, including the fact that BMD changes are a known side effect of weight loss itself. They contextualized the safety finding within broader positive results.

Viking faced a different challenge when its oral VK2735 showed strong efficacy but a higher discontinuation ate – news that resulted in a 35% drop in their stock price. Viking reframed the issue around dose-dependent tolerability, longer-term maintenance strategy, and the convenience of a once-daily pill. They transformed a potential weakness into a unique value proposition.

This isn't just crisis management, it's narrative control. It shows up across the narrative but most heavily in Commitments - how companies contextualize setbacks, set expectations, and keep key stakeholder audiences with them.

Why This Matters

In this new GLP-1 landscape, up-and-comers don't need to simply match the efficacy numbers of Lilly and Novo. Instead, they must establish clear, differentiated narratives that anticipate and address the market's deeper concerns about real-world adherence, safety, and long-term value.

For MariTide and VK2735, their stories are early signals of breaking through the noise. So far, both are meeting the narrative moment, with more room to improve as trials progress. Their ability to control and defend their narratives is proving to be as critical as the clinical data itself.

As always, the science remains paramount, and most drugs fail regardless of their story. But in a soon-to-be $100 billion market where multiple viable treatments will coexist, narrative clarity, credibility, and resilience are competitive assets that determine who captures sustained market share.

The story war in GLP-1s is just beginning. And the companies that understand story is strategy will be the ones serving the most patients as the market matures.