The GLP-1 Narrative: Lilly vs. Novo in the War of the Words

The $63B GLP-1 market is about stories as much as receptors.

GLP-1 drugs are battling for attention in clinics, on Wall Street, and in the more subtle arena of the story itself. And if you ask most people who’s winning hearts and minds right now, their instinctive answer is Lilly with Zepbound and Mounjaro.

But in a $63 billion market projected to reach $100 billion in 2030, intuition about the story isn’t enough. So I ran all four GLP-1s through my Signal Score™ diagnostic to find out what the “story data” say.

Looking at Lilly’s Zepbound and Mounjaro versus Novo Nordisk’s Ozempic and Wegovy, the numbers show Lilly nudging ahead in narrative clarity, credibility, and resonance. The scores are close, with Zepbound (84/100), Mounjaro (81/100), Wegovy (78/100) Ozempic (75/100), but Lilly’s dual-receptor positioning is clearly “out-narrating” Novo’s heritage story.

The method behind the diagnostic

How do you measure something as slippery as “story”? In this case, I narrowed the inputs down to three of the strongest, most widespread signals a company sends about its brands:

Product homepage: the polished story the manufacturer wants the world to see.

Press releases (2025 only): the emphasis and rhythm of what the companies choose to talk about.

Package insert (PI): the sober, regulator-facing truth.

Taken together, these sources let us compare apples to apples (or… semaglutides to tirzepatides). Each is consistent across all four products and carries weight with different audiences. Together they reveal what the companies are saying, and how closely their public story aligns with what they tell regulators.

The Lilly narrative advantage

Before diving into the details, let’s look at the big picture: Lilly’s dual GIP/GLP-1 receptor story creates narrative advantage. Novo talks about optimizing single-pathway GLP-1 therapy, but Lilly positions breakthrough innovation that makes existing treatments look outdated.

In this case, it’s not necessarily about “better science,” but about better positioning of science in the storytelling.

Let’s look at how the stories are being told.

Decoding press releases

One of the clearest windows into what a company wants the world to notice, press releases for pharmaceuticals are required by regulators for label changes or safety updates. But press releases are often discretionary for actions like highlighting head-to-head wins, launching patient programs, amplifying access initiatives. That’s where drug manufacturers show their real story emphasis.

Zepbound has been the “louder” brand in 2025, with multiple press releases from Lilly focused on access and affordability (new vial options, self-pay programs) and, crucially, head-to-head data against Wegovy showing superior 20.2% vs 13.7% weight loss. Mounjaro, by contrast, has just one major 2025 press release so far -- a mandatory(ish) trial outcomes disclosure. That difference matters: Zepbound’s releases are proactive and market-shaping, while Mounjaro’s is more reactive and data-focused. Together they show Lilly’s chips are stacked behind Zepbound as a product and as a flagship story.

Why the PI matters

This part is especially interesting to me. Package inserts may be the driest of documents, but they’re also the truest. They’re the voice of a company talking to regulators, with no room for flourish, theme songs, or other narrative embellishment. By comparing the PI against the brand website and press releases, you see the gaps where marketing pushes harder, where science may be softened, or where emphasis shifts.

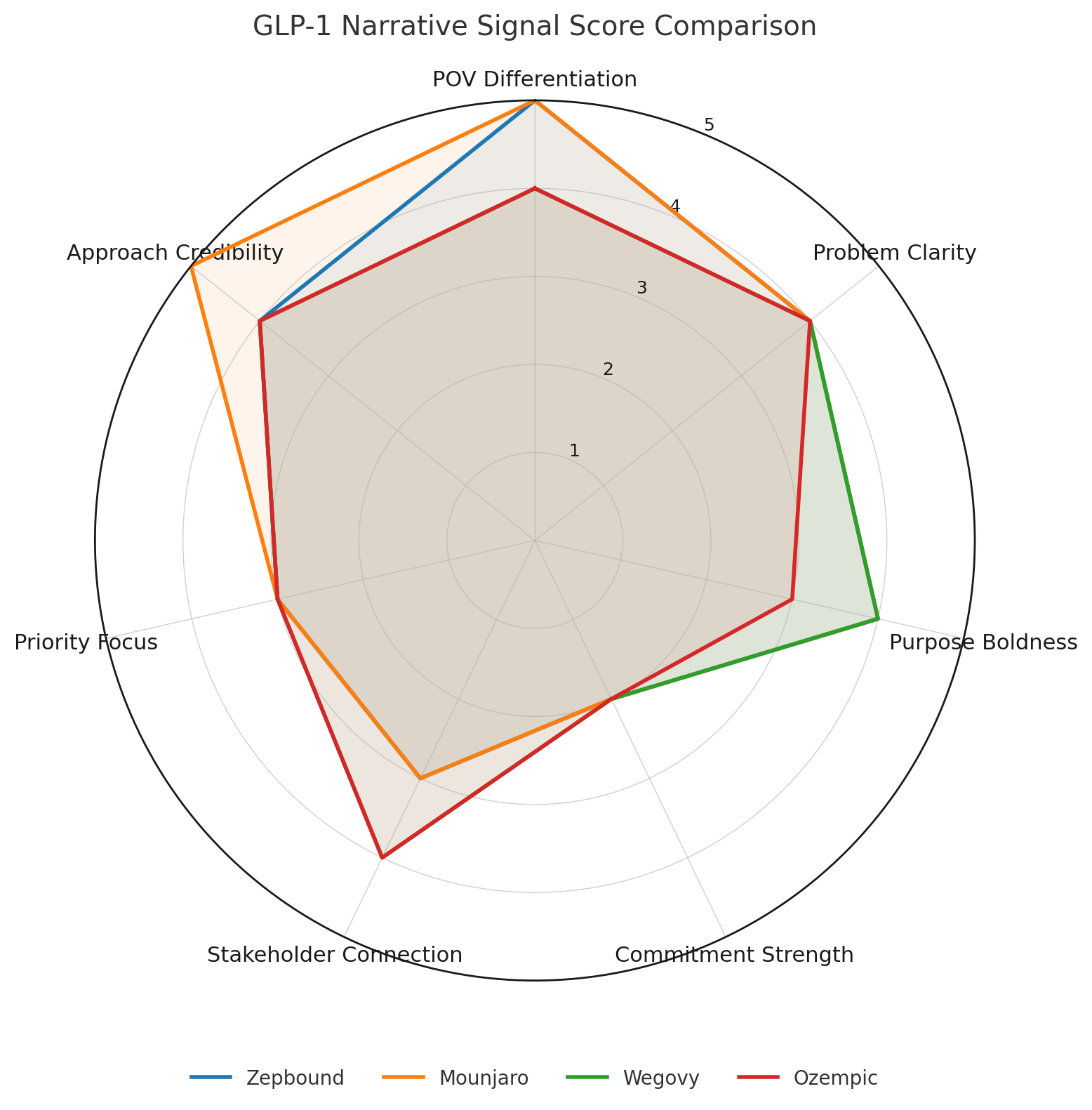

The Signal Score™ diagnostic

I scored each product’s narrative across seven dimensions: purpose boldness, problem clarity, point-of-view differentiation, approach credibility, priority focus, stakeholder connection, and commitment strength. Each weighted, totaled to 100.

Here’s what those categories look like when you take a closer look at the brand language:

Zepbound (Lilly) 84/100

Purpose: Delivers “superior weight loss outcomes through breakthrough dual-receptor innovation.” Clear and bold, positioning itself as a category-definer.

Commitments: Patient access front and center, with repeated pledges to expand affordability through LillyDirect and self-pay programs.

Standout strength: Perfect POV differentiation (20/20) through genuine therapeutic breakthrough.

Mounjaro (Lilly) 81/100

Approach: Positioned as the dual-agonist diabetes drug that can “redefine diabetes treatment” by delivering superior glycemic control and weight reduction.

Commitments: Less about access, more about proving credibility with regulators and physicians.

Standout strengths: Perfect POV differentiation (20/20) and Approach credibility (15/15).

Wegovy (Novo Nordisk) 78/100

Purpose: Framed around transforming obesity treatment through “clinically meaningful weight loss that reduces cardiovascular risk.” A bit vague, lacking clear positioning.

Problem: Emphasizes the scale of obesity as a public health crisis. Credible, but not particularly differentiated.

Ozempic (Novo Nordisk) 75/100

Approach: “Proven semaglutide therapy through once-weekly injections” providing comprehensive diabetes protection. Credible, with heavy emphasis on its already-iconic brand status.

Commitments: Implicit rather than explicit, mostly about maintaining safety and tolerability.

The result: Lilly’s dual-receptor approach creates clear narrative advantages. Their breakthrough innovation story makes Novo’s existing treatments look like yesterday’s technology. Both Zepbound and Mounjaro from Lilly score higher overall than Ozempic and Wegovy, and dominate in POV differentiation, the dimension that matters most for cutting through market noise.

Soft on Commitments, but that hurts only one company

One of the more revealing findings is that all four products struggle with Commitment strength (4-6/10), but Lilly’s innovation positioning and POV makes this dimension less critical for them. Stakeholders expect bold science claims when you’re promising breakthrough therapy. When you’re promising heritage and reliability, though, they expect bold commitments. In this context, Novo’s weaker commitment scores hurt them more.

Why this matters

This isn’t just academic. Stories shape markets, and narrative advantages translate directly to market share. A company that tells a bold, credible story wins trust faster, sustains attention longer, and lays the groundwork for the next launch or label expansion.

In this GLP-1 race, science alone won’t decide the winner. Narrative will, too. And right now, Lilly’s story is landing with more force.

Which is exactly what a good narrative should do.